Removing obstacles on tax refund

| Over 2.4 million transactions of online tax payment have been made | |

| Further expanding e-tax refund in 2018 | |

| The Taxation has handled 2, 317 e-tax refund dossiers |

|

| Customs officers of Cau Treo border gate Customs Branch (Ha Tinh) inspect imports and exports. Photo: H. Nu |

Dong Thap Tax Department reflected that procedures of Customs clearance and VAT refund for the food industry is not as clear as the by-products of the food industry such as broken rice, rice husk and bran, etc.

Regarding this, the GDC said that the Customs procedures are currently implemented in accordance with the Customs Law, Decree No. 08/2015 / ND-CP of the Government and Circular No. 38/2015 / TT-BTC of the Ministry of Finance. The above-mentioned documents have specifically guided the implementation of Customs goods clearance procedures. The unit is requested to follow the above documents for implementation.

For VAT for food industry by-products, such as broken rice, bran and rice husk, on 31st October 2014, the Ministry of Finance issued Official Letter No. 15895 / BTC-CST guiding the VAT on cultivation products. Accordingly, wheat bran and rice bran (derived from the milling process of paddy or wheat) are discarded cultivation products and by-products, and are identified as unprocessed products into other products as described at Point b1, Clause 3 of Article 4 of Circular No. 83/2014 / TT-BTC. Hence, broken rice, bran and rice husk shall not be subject to VAT at the stage of self-production for consumption and importation and shall not be subject to VAT declaration, calculation and payment at the stage of trading under the guidance in Clause 1 of Article 4 and Clause 5 of Article 5 of Circular No. 219/2013 / TT-BTC and Point b1, Clause 3 of Article 4 of Circular No. 83/2014 / TT-BTC.

If enterprises deduct the input VAT refund for food industry by-products, such as broken rice, bran and rice husk, they shall contact the local tax offices for guidance and settlement. If enterprises make wrong payments and over payments of VAT for imported goods above, they must contact the Customs authority for guidance in accordance with Circular 38/2015/TT-BTC.

ABB Company Ltd asked about exporting some transformers to foreign markets, including the machinery body and accessories. In certain cases, the company has to ship the machinery body first and then send accessories later in the next shipment. However, these accessories are not considered for tax refund.

The GDC answered that pursuant to Clause 1, Article 19 of the Law on import and export duties, the cases of tax refund shall include:

“a) Tax payers have paid import or export duty but there is no imported or exported goods; or taxpayers have overpaid import or import duty;

b) Taxpayers have paid export duty but the exported goods which is re-imported shall be refunded the paid export duty and shall not subject to import duty.

c) Taxpayers have paid import duty but the imported goods which is re-exported shall be refunded the paid import duty and shall not be subject to export duty.

d) Taxpayers have paid import duty for goods imported for production and business but the imported goods is used for export production”

Also, the Clause 2 of Article 19 of Law on Import and Export duties stipulates that “Goods prescribed in point a, b and c of Clause 1 of this Article shall be subject to tax refund if they have not been used and processed”.

The Clause 1 of Article 34 of Decree No. 134/2016/ND-CP of the Government regulates that imports that have paid import duties shall be subject to the import duty refund and shall not pay the export duty. Accordingly, taxpayers who have paid imported duty on imported goods for production and business but used those goods for export production and export to foreign countries or to non-tariff areas shall be refunded the paid import duty.

Clause 1 of Article 34 of Decree No. 134/2016 / ND-CP of the Government stipulates that imported goods that have paid import duties but have to be re-exported shall be subject to import duty refund and shall not pay export duty. Accordingly, taxpayers who have paid import duty on imported goods for production and business, but used those goods for export production and export to foreign countries or to non-tariff areas, shall be refunded the paid import duty.

The basis for determination of eligibility for duty refund and an application of duty refund are in accordance with the provisions of Clause 3 and 5 of Article 36 of Decree No. 134/2016 / ND-CP.

The GDC requests enterprises to study the above regulations for implementation. In case of any problems, the enterprises shall contact the customs offices where the declarations are registered for specific guidance or submit their dossiers to the GDC for consideration and settlement.

Felix Metal Tech Co., Ltd (Hai Phong) asked, are discarded materials that are collected from the production process and in production norms, with import origin but then exported (registered declaration in Customs regime B11) exempt from export duty as stipulated in Clause 5, Article 114 of the Ministry of Finance's Circular No. 38/2015 / TT-BTC dated 25th March 2015?

The company also requested the GDC to give specific guidance on the case whether the company has to pay the export duty for discarded materials that were obtained from the export production of imported materials when exporting them or not? (Divided in 2 periods: the first period from 1st September 2016 and earlier and the second period from 1st September 2016 onwards.

Concerning the above question, the GDC (the Department of Import-Export Duties) has sent an Official Letter No. 4477 / TXNK-CST dated 15th November to reply to Hai Phong Customs Department on dealing with exported duty for discarded materials obtained from the export production of imported materials of Felix Metal Tech Co., Ltd

Specifically before 1st September 2016: The GDC issued Official Letter No. 5334 / TCHQ-TXNK dated 8th June 2016, guiding the implementation as follows: Pursuant to Clause 4 of Article 15 of the Government’s Decree 87/2010 / ND -CP dated 13th August 2010, Clause 5 of Article 114 of the Ministry of Finance's Circular No. 38/2015 / TT-BTC dated 25th March 2015,

Imported goods on which import tax has been paid that are used for export production to foreign counties or non-tariff areas shall receive a tax refund in proportion to the quantity of exported goods. Export tax on exported goods is exempt if there is ample basis to determine that such goods are made entirely of imported materials.

Pursuant to Clause 3 of Article 128 of the Ministry of Finance's Circular No. 38/2015 / TT-BTC of 25th March 2015: If there is ample basis to determine that exported goods are entirely processed of imported materials which are not subject to export tax, the application for export tax exemption shall consist of:

a) 01 original copy of the written request for exemption from export tax if goods are made entirely of imported materials, which specifies:

a.1) The number of the declaration of exported goods on which tax is to be exempted; goods names, line numbers, quantity of goods on the Customs declaration (in case of exemption of part of the tax on the Customs declaration); number of the declaration of imported goods; number of the contract related to the exported goods on which tax is to be exempted;

a.2) Quantity of imported materials used for export production and process;

a.3) The amount of export tax to be exempted;

According to the company’s question, the company imported 100% stainless steel materials from abroad to produce export products including stainless steel scrap. The company assured that the stainless steel scrap was obtained from production and originated 100% from imported raw materials and was not originated from mineral resources exploited in Vietnam. Therefore, the company is requested to submit import dossiers of stainless steel, export dossiers of stainless scrap to the Customs office where the export procedures are done to check and handle in accordance with the above regulations.

| The Taxation refunded more than 26 trillion VND via application of electronic tax refund VCN – The Taxation is actively applying information technology in the implementation of projects and tasks to ... |

According to the GDC, from 1st September 2016, the tax exemptions are specified in Article 16 of the Law on Import and Export Duties; from Article 5 to Article 29 of Decree No. 134/2016 / ND-CP of the Government. In which the tax exemption for raw materials, supplies and components imported to export production is regulated in Clause 7 of Article 16 of the Law on Import and Export Duties; and Article 12 of Decree No. 134/2016 / ND-CP which does not stipulate the exemption from export tax on goods as discarded materials obtained from export production of imported materials.

Customs newspaper will continue to provide information on solving tax refund problems in the following publications.

Related News

Customs sector strengthens anti-smuggling for e-commerce products

19:09 | 21/12/2024 Anti-Smuggling

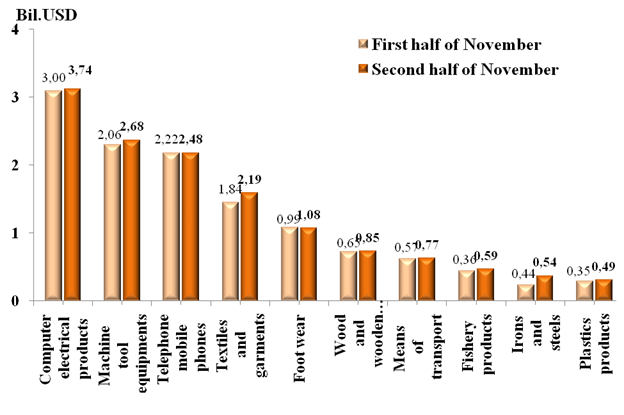

Preliminary assessment of Vietnam international merchandise trade performance in the second half of November, 2024

15:18 | 19/12/2024 Customs Statistics

Achievements in revenue collection are a premise for breakthroughs in 2025

09:57 | 18/12/2024 Customs

Numerous FDI enterprises face suspension of customs procedures due to tax debt

09:57 | 18/12/2024 Anti-Smuggling

Latest News

Minister of Finance Nguyen Van Thang: Facilitating trade, ensuring national security, and preventing budget losses

19:09 | 21/12/2024 Customs

Official implementation of the program encouraging enterprises to voluntarily comply with Customs Laws

18:31 | 21/12/2024 Customs

Proactive plan to meet customs management requirements at Long Thanh International Airport

18:30 | 21/12/2024 Customs

An Giang Customs issues many notes to help businesses improve compliance

09:29 | 20/12/2024 Customs

More News

Hai Phong Customs processes over 250,000 declarations in November

15:18 | 19/12/2024 Customs

Binh Duong Customs surpasses budget revenue target by over VND16.8 Trillion

09:39 | 18/12/2024 Customs

Director General Nguyen Van Tho: Customs sector strives to excellently complete 2025 tasks

16:55 | 17/12/2024 Customs

Customs sector deploys work in 2025

16:43 | 17/12/2024 Customs

Mong Cai Border Gate Customs Branch makes great effort in performing work

11:23 | 16/12/2024 Customs

Declarations and turnover of imported and exported goods processed by Lao Bao Customs surge

09:17 | 15/12/2024 Customs

General Department of Vietnam Customs prepares for organizational restructuring

19:28 | 14/12/2024 Customs

Revenue faces short-term difficulties but will be more sustainable when implementing FTA

19:27 | 14/12/2024 Customs

Customs sector collects over VND384 trillion in revenue

17:13 | 12/12/2024 Customs

Your care

Minister of Finance Nguyen Van Thang: Facilitating trade, ensuring national security, and preventing budget losses

19:09 | 21/12/2024 Customs

Official implementation of the program encouraging enterprises to voluntarily comply with Customs Laws

18:31 | 21/12/2024 Customs

Proactive plan to meet customs management requirements at Long Thanh International Airport

18:30 | 21/12/2024 Customs

An Giang Customs issues many notes to help businesses improve compliance

09:29 | 20/12/2024 Customs

Hai Phong Customs processes over 250,000 declarations in November

15:18 | 19/12/2024 Customs