VAT expected to reduce to 8% from early February

| Ho Chi Minh City's economic motivation from import and export activities | |

| Centralized exchange helps to clean up corporate bond market | |

| Gifts not subject to tax incentives under Resolution 106 |

|

| Goods and services subject to 10% tax will enjoy a 2% VAT reduction |

Some goods and services will not be eligible VAT reduction

According to the draft, the 2% VAT reduction will be applicable to goods and services which are currently subject to the 10% tax rate from the date this Decree comes into force until the end of December 31, 2022, except for the following cases:

Telecommunications, financial activities, banking, securities, insurance, real estate trading, metals and prefabricated metal products, mining products (excluding coal), coke, refined petroleum, chemicals and chemical products; products, goods and services subject to special consumption tax; information technology under the law on information technology.

Details of items and services that are not eligible for VAT reduction mentioned above shall comply with Appendices 1 and 2 attached to the Decree.

For the items and services which are not subject to VAT or subject to 5% VAT, the VAT law shall be applied.

Regarding the VAT deduction, the draft decree states that business establishments that calculate VAT by the deduction method may apply the VAT rate of 8% for goods and services mentioned above.

Business establishments that calculate VAT according to the percentage method on revenue are entitled to a 20% reduction of the percentage rate to calculate VAT on goods and services specified above.

Procedures detailed in the Decree

In the draft, the Ministry of Finance also specifies procedures. Accordingly, for business establishments mentioned above, when making VAT invoices providing goods and services subject to VAT reduction, in the VAT line, fill "the prescribed tax rate of 8%"; VAT amount; and the total amount to be paid by the buyer.

Based on VAT invoices, business establishments who provide goods and services shall declare output VAT, and business establishments who purchase goods and services shall declare deductions of input VAT according to the reduced tax stated on the VAT invoice.

For business establishments specified in Point b, Clause 2 of this Article, when making invoices for providing goods and services eligible for VAT reduction, in the column “amount” write all the money for goods and services before the reduction, in the column “goods and services", write the amount that has reduced 20% to calculate VAT according to Resolution 43.

For business households and individuals who pay tax according to the presumptive method, the tax agency shall determine the VAT according to the principle of 20% reduction of the percentage rate to calculate VAT on goods and services specified in Clause 1.

In case the organization declares or pays on its behalf, the VAT shall be determined on the tax declaration, ensuring the principle of reducing 20% of the percentage rate for tax calculation and the taxpayer shall make a table to determine the reduced VAT amount according to the form attached to the decree.

For business establishments providing many goods and services, they shall issue a separate invoice for the goods eligible for VAT reduction.

If the business establishment has issued an invoice and declared at the tax rate or percentage to calculate the value added tax that has not yet been reduced, the seller and the buyer must make a record or reach a written agreement that states the errors and the seller issues an invoice to correct the error and delivers it to the buyer.

Based on the revised invoice, the seller declares the revised output tax, and the buyer declares the revised input tax (if any).

Business establishment providing goods and services eligible for VAT reduction has issued pre-printed invoices with a value that has not yet been used up and the business establishment has a need to continue using them, they shall make stamps of 2% VAT reduction on price or the 20% of the percentage rate on the price next to the pre-printed reduction criteria for continued use.

| Are there any risks when the Customs office refunds the overpaid Value Added Tax at the import stage? |

The Ministry of Finance expects that the VAT reduction policy will reduce state budget revenue in 2022 by about VND49.4 trillion.

Related News

Stimulate production and business, submit to the National Assembly to continue reducing 2% VAT

15:47 | 02/12/2024 Finance

Goods trading, being seen from Lang Son border gate

13:45 | 28/11/2024 Customs

7 key export groups bring in US$234.5 billion

13:54 | 28/11/2024 Import-Export

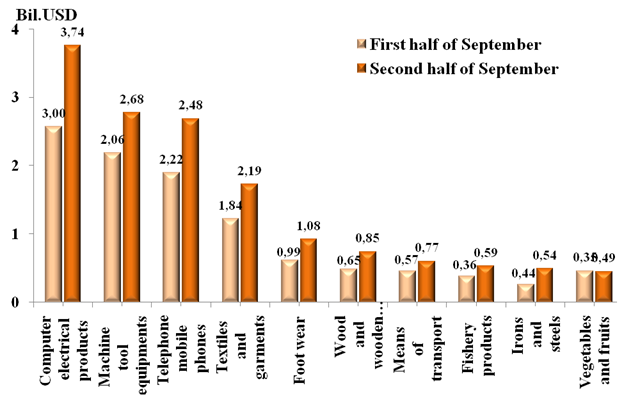

Preliminary assessment of Vietnam international merchandise trade performance in the second half of September, 2024

09:21 | 20/11/2024 Customs Statistics

Latest News

Resolve problems related to tax procedures and policies for businesses

13:54 | 22/12/2024 Regulations

New regulations on procurement, exploitation, and leasing of public assets

09:17 | 15/12/2024 Regulations

Actively listening to the voice of the business community

09:39 | 12/12/2024 Customs

Step up negotiations on customs commitments within the FTA framework

09:44 | 08/12/2024 Regulations

More News

Proposal to amend regulations on goods circulation

13:45 | 06/12/2024 Regulations

Review of VAT exemptions for imported machinery and equipment

10:31 | 05/12/2024 Regulations

Customs tightens oversight on e-commerce imports

13:39 | 04/12/2024 Regulations

Bringing practical experience into customs management policy

13:48 | 03/12/2024 Regulations

Businesses anticipate new policies on customs procedures and supervision

15:41 | 29/11/2024 Regulations

Amendments to the Value-Added Tax Law passed: Fertilizers to be taxed at 5%

13:43 | 28/11/2024 Regulations

Proposal to change the application time of new regulations on construction materials import

08:52 | 26/11/2024 Regulations

Ministry of Finance proposed to reduce VAT by 2% in the first 6 months of 2025

09:00 | 24/11/2024 Regulations

Hanoi Customs resolves tax policy queries for enterprises

09:26 | 22/11/2024 Regulations

Your care

Resolve problems related to tax procedures and policies for businesses

13:54 | 22/12/2024 Regulations

New regulations on procurement, exploitation, and leasing of public assets

09:17 | 15/12/2024 Regulations

Actively listening to the voice of the business community

09:39 | 12/12/2024 Customs

Step up negotiations on customs commitments within the FTA framework

09:44 | 08/12/2024 Regulations

Proposal to amend regulations on goods circulation

13:45 | 06/12/2024 Regulations