Exchange rate sees flexible fluctuations

.") |

| Assoc. Prof. Dr. Ngo Tri Long, former director of the Price and Market Research Institute (Ministry of Finance). |

How do you assess the impact of the world market on the domestic foreign currency market?

The US Federal Reserve (Fed) decided to increase the basic interest rate by 0.5% points, to 0.75%-1%. This is the highest interest rate increase since May 2020 to curb inflation.

In addition, inflationary pressure in many countries will also affect the macroeconomic situation, including the foreign currency market in Vietnam.

However, the exchange rate in Vietnam for many years has been flexibly governed by the State Bank of Vietnam (SBV) according to market developments, trade balance, payment balance as well as movements of key foreign currencies in the reference basket.

Moreover, the impacts from the domestic and international markets have been forecast by the management agencies, so they should be proactive in dealing with any fluctuations. Therefore, the foreign exchange rate in Vietnam is affected but not much, and does not see devaluation like many countries in the region and in the world.

The main reason is that the domestic macroeconomy is kept stable, creating safe "buffers" for the exchange rate against strong fluctuations from outside. Specifically, Vietnam's foreign exchange reserves are reaching a relatively high level (over US$110 billion), the supply of foreign currencies such as remittances and FDI disbursement is forecast to grow steadily, and the trade balance of the first four months is expected to see a surplus of US$2.53 billion that will expand for the whole year.

Moreover, the consumer price index (CPI) and inflation in Vietnam have remained low, so the regulators may not use the tight monetary policy tool. In my opinion, the USD exchange rate in Vietnam in 2022 will fluctuate between 0.8-1.6% compared to 2021.

The fact that the domestic USD exchange rate since the beginning of the year has only fluctuated around 0.8% while other currencies have depreciated by 3-4%, even at a higher level, which is beneficial for exporters but does this pose any problems in the management of the domestic foreign exchange market?

Although the exchange rate in Vietnam has a lower devaluation rate than many other foreign currencies, our country’s exchange rate is not at a fixed level, but the exchange rate is flexibly regulated by the State Bank of Vietnam according to daily market movements. If Vietnam's exchange rate remains at a fixed level as current, it will harm itself, affect the competitiveness of the economy, and even fall into doubt of currency manipulation.

But the current low volatility of the domestic foreign exchange rate is beneficial to export activities, because the low level of devaluation will help improve the value of goods of Vietnamese enterprises.

In the long run, the movement of the foreign exchange rate in our country is still not worrisome, because we have many "buffers" to help stabilize the exchange rate. Because of the high risk of inflation, exchange rate fluctuations are also one of the important indicators of inflation, so a high exchange rate will have a great impact on the macroeconomy.

In addition, Vietnam's flexible and stable exchange rate management is still highly appreciated by many international organizations. The US Department of Finance has removed Vietnam from the list of currency manipulators due to meeting the criteria of bilateral trade surplus with the US, current account surplus and foreign currency intervention.

In your opinion, under pressure from inflation, how will the management agency manage monetary policy in the near future?

There are still many pressures that make it difficult for inflation control target this year. In particular, import inflation is expected to surge due to factors such as major trading partners, who are experiencing record-high inflation, will continue to increase large demand stimulus packages; the pandemic has been complicated.

In addition, inflationary pressure also comes from the ability to adjust items managed by the State. The strong implementation of the Economic Recovery Support Program for the 2022-2023 period will also increase the money supply and expand inflation in those two years and possibly in the following year.

Therefore, the management of monetary policy must have necessary scenarios in the direction of tightening, especially for the inflation control target of below 4%.

| Reference exchange rate up 4 VND The State Bank of Vietnam set the daily reference exchange rate at 23,148 VND per USD on ... |

Therefore, in the near future, it is necessary to improve efficiency in coordinating fiscal and monetary policies in managing the money supply, interest rates, neutralizing money in and out and regulating prices. At the same time, Vietnam should improve the efficiency of the implementation of the socio-economic recovery program, including support packages for people and businesses, and demand and supply stimulus packages, thereby directing cash flow into areas with strong recovery potentials and high pervasiveness.

Related News

Flexible and proactive when exchange rates still fluctuate in 2025

11:03 | 30/12/2024 Finance

Managing price effectively, reducing pressure on inflation

12:09 | 04/10/2024 Finance

Pressure on exchange rate plunges

18:02 | 01/09/2024 Finance

Inflationary pressure seen from monetary policy

09:47 | 21/07/2024 Finance

Latest News

SBV makes significant net withdrawal to stabilise exchange rate

07:59 | 15/01/2025 Finance

Việt Nam could maintain inflation between 3.5–4.5% in 2025: experts

06:19 | 11/01/2025 Finance

Banking industry to focus on bad debt handling targets in 2025

14:38 | 03/01/2025 Finance

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

More News

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance

Tax policies drive strong economic recovery and growth

07:55 | 31/12/2024 Finance

E-commerce tax collection estimated at VND 116 Trillion

07:54 | 31/12/2024 Finance

Big 4 banks estimate positive business results in 2024

13:49 | 30/12/2024 Finance

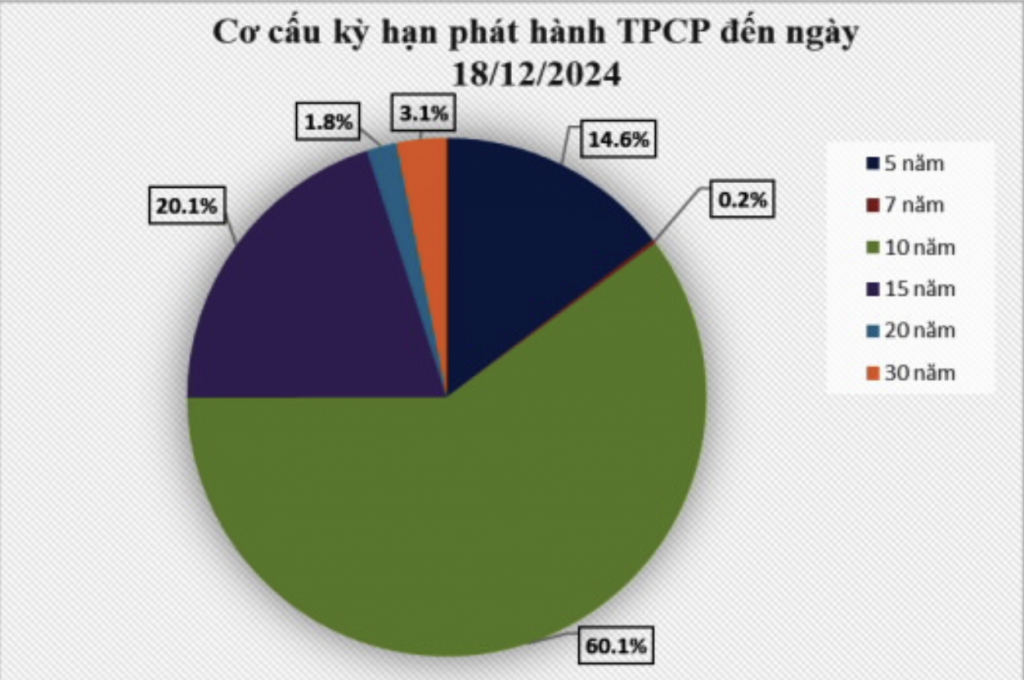

Issuing government bonds has met the budget capital at reasonable costs

14:25 | 29/12/2024 Finance

Bank stocks drive market gains as VN-Index closes final Friday of 2024 on a positive note

17:59 | 28/12/2024 Finance

Banks still "struggling" to find tools for handling bad debt

13:47 | 28/12/2024 Finance

Forecast upbeat for banking industry in 2025

14:30 | 27/12/2024 Finance

Ensuring financial capacity of bonds issuers

11:09 | 26/12/2024 Finance

Your care

SBV makes significant net withdrawal to stabilise exchange rate

07:59 | 15/01/2025 Finance

Việt Nam could maintain inflation between 3.5–4.5% in 2025: experts

06:19 | 11/01/2025 Finance

Banking industry to focus on bad debt handling targets in 2025

14:38 | 03/01/2025 Finance

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance