Bad debt is not a concern for the growth of banks

| Law on bad debt settlement urgently needed: experts | |

| Bad debt worries to ease thanks to high provision rate | |

| Directing cash flow to priority areas, preventing bad debts from increasing |

|

| Mr Dang Tran Phuc |

How do you forecast bank profits in 2022?

In 2022, AzFin forecasts that the banking industry's business results will still be very positive with the growth of profit after tax of the whole industry from 20-25% compared to 2021.

This forecast is determined on three factors. Firstly, credit growth is forecast to be quite high, about 14% when the economy opens, businesses will return faster and stronger than during the 2009-2013 crisis. The industry has had a long period of good business development and accumulated financial resources from 2014 to 2020, and the Government manages this effectively. Credit demand has grown stronger than in 2021.

Secondly, banks are increasingly exploiting their customer base with many non-credit products and services, bringing profits and accounting for a higher proportion of the bank's income structure, contributing to promoting high-profit growth. Third, the trend of digitization and reduction of cash makes people use more banking services. In addition, the application of technology helps banks reduce personnel and transportation costs, thereby increasing profits.

What will be the adverse factors affecting the banking industry?

Inflation and interest rates in developed countries like the US and Europe are at very high levels, which can partly "export inflation" to other countries like Vietnam. Besides, this will create a psychological impact on depositors, causing banks to increase input deposit interest rates, leading to a decrease in net interest income (NIM) in a short period of time, some banks failed to increase demand deposit ratio (CASA).

In recent days, political tensions between Russia and Ukraine have also partly caused instability, causing them to shift from depositing banks to taking refuge in gold and real estate thus banks may have to slightly raise interest rates to attract deposits.

Accelerated credit will be accompanied by a high risk of bad debt and increased provision for risks. Is this a concern for banks this year, sir?

We believe that the absolute amount of bad debts will increase with credit growth, but the relative number (percentage of on-balance sheet bad debt and potential debt) of banks in 2022 will not be concerns and the business results of banks will not be affected. This is due to the following reasons:

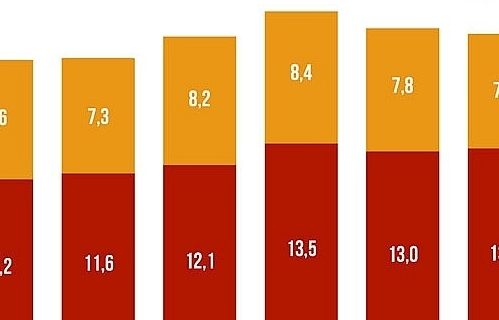

Firstly, the capacity and quality of risk management, especially the appraisal stage of banks have improved, which will limit the increase in bad debts. It is clear that through the 2020-2021 period, despite the impact of the Covid-19 pandemic causing difficulties for people and businesses, the bad debt ratio of banks remained at a very low level, 1.76% and 1.92% of total outstanding loans, equivalent to 2018 and only a third of the crisis period of 2011-2013.

Second, loans are currently mostly secured by real estate, given the sharp increase in real estate prices and the loan-to-secured ratio that AzFin estimates is only 50-60%, the risk of losing capital is not high, making the cost of provision as well as bad debt handling low.

Third, thanks to the fact that the economy has reopened to almost normal before the pandemic, even the most impacted industries such as tourism, hotels, and airlines are gradually returning, since the end of the fourth quarter of 2021 a lot of borrowers subject to restructuring debt have returned to normal business activities, meaning the risk of a sharp increase in bad debts after the State Bank's postponement of provisioning for restructuring debts ends in mid-2022 will not occur.

Fourth, most banks have actively set up very high provisions for bad debts for 2021. This will be a very good buffer to reduce costs or at least not significantly increase provision expenses for bad debts.

On the other hand, many banks, from private banks to state-owned commercial banks, have been boosting revenue from the retail segment. The retail segment is not only attractive because of its high growth, but also because of its very high profit margin (usually NIM is two times higher than that of the wholesale segment), exploiting and cross-selling many value-added products and services along with high distribution. Spreading to millions of customers makes the risk of loss much lower than credit.

With the above assessment, could you please tell us what the prospect of banking stocks will be from now to the end of the year?

We assess the outlook for bank stocks for 2022 as quite good with the expectation that this sector's stock price can grow at a rate of about 20-25%. However, we think that 2022 will be a "quiet" year for this sector, so there will not be many "items" to help the stock price increase like in 2021.

However, news related to issuing to foreign investors, selling capital in subsidiaries, being granted higher credit growth limits or dealing with bad debts can create strong short-term waves.

Along with that, the high dividend payment in shares and the expansion of foreign room, the issuance of shares to increase capital is forecast by banks to continue to be promoted in 2022 due to large expansion and development needs. This will help banks increase equity capital, thereby increasing the capital adequacy ratio (CAR) to meet Basel III standards and help the banking industry develop more sustainably. These issues will contribute to good growth in bank stock prices in the medium and long term.

Thank you Sir!

Related News

Top 10 Reputable Animal Feed Companies in 2024: Efforts to survive the challenges of nature

18:30 | 21/12/2024 Import-Export

There is still room for credit growth at the end of the year

09:43 | 08/12/2024 Finance

Ho Chi Minh City achieves record state revenue of over VND500 trillion in 2024

10:33 | 10/12/2024 Finance

Vietnam's GDP growth forecast raised due to strong recovery trend

15:48 | 02/12/2024 Headlines

Latest News

Nghệ An Province anticipates record FDI amidst economic upswing

15:49 | 26/12/2024 Import-Export

Green farming development needs supportive policies to attract investors

15:46 | 26/12/2024 Import-Export

Vietnamese enterprises adapt to green logistics trend

15:43 | 26/12/2024 Import-Export

Paving the way for Vietnamese agricultural products in China

11:08 | 26/12/2024 Import-Export

More News

VN seafood export surpass 2024 goal of $10 billion

14:59 | 25/12/2024 Import-Export

Exporters urged to actively prepare for trade defence investigation risks when exporting to the UK

14:57 | 25/12/2024 Import-Export

Electronic imports exceed $100 billion

14:55 | 25/12/2024 Import-Export

Forestry exports set a record of $17.3 billion

14:49 | 25/12/2024 Import-Export

Hanoi: Maximum support for affiliating production and sustainable consumption of agricultural products

09:43 | 25/12/2024 Import-Export

Việt Nam boosts supporting industries with development programmes

13:56 | 24/12/2024 Import-Export

VN's wood industry sees chances and challenges from US new trade policies

13:54 | 24/12/2024 Import-Export

Vietnam's fruit, vegetable exports reach new milestone, topping 7 billion USD

13:49 | 24/12/2024 Import-Export

Aquatic exports hit 10 billion USD

13:45 | 24/12/2024 Import-Export

Your care

Nghệ An Province anticipates record FDI amidst economic upswing

15:49 | 26/12/2024 Import-Export

Green farming development needs supportive policies to attract investors

15:46 | 26/12/2024 Import-Export

Vietnamese enterprises adapt to green logistics trend

15:43 | 26/12/2024 Import-Export

Paving the way for Vietnamese agricultural products in China

11:08 | 26/12/2024 Import-Export

VN seafood export surpass 2024 goal of $10 billion

14:59 | 25/12/2024 Import-Export