Assessing budget revenues in 2022

| Impressive growth in budget revenue | |

| Customs stands side by side with businesses to overcome difficulties | |

| Khanh Hoa Customs assists enterprises and raises budget revenue |

|

| Tax officers of Thai Nguyen Tax Department at work. Photo: General Department of Taxation |

Accordingly, the General Department of Taxation requires that tax departments fully review and evaluate the impact of each policy on each revenue and tax when assessing budget revenues in 2022.

Accordingly, in addition to assessing the direct impact of increasing/decreasing state budget revenue, it is necessary to evaluate the indirect effects on economic growth and other taxes.

Specifically, the Tax authority shall focus on evaluating the efficiency of issued policies to support businesses and people affected by the Covid-19 pandemic and policies to support the recovery of enterprises, cooperatives and business households.

The tax authority shall assess policies issued in 2021 but their impacts continue to 2022 such as Resolution 1148/2020/UBTVQH14 dated December 21, 2020 of the National Assembly Standing Committee amending and supplementing subsection 2, section I, of the Green Tax Schedule; Decree 44/2021/ND-CP dated March 31, 2021 of the Government guiding the implementation of deductible expenses when determining taxable income for enterprises for expenditures for supporting or sponsoring for Covid-19 pandemic prevention and control activities, applicable to the corporate income tax period of 2020 and 2021; and Decree 52/2021/ND-CP dated April 19, 2021 of the Government on the extension of payment deadlines for taxes and land rent.

The local Tax Departments shall also summarize the amount of corporate income tax in the first and second quarters of 2021 of businesses that have a fiscal year other than the calendar year and are extended for tax payment in 2022; assess impacts on revenue in 2022 (if any) for the cases covered by Clause 4, Article 5 of Decision 27/2021/QD-TTg on the reduction of land rent in 2021 for those affected by the Covid-19 pandemic.

At the same time, it is necessary to calculate the 30% reduction of the tax payable of the 2021 corporate income tax period for enterprises that have a turnover in the 2021 tax period not exceeding VND200 billion and lower than the revenue in the 2019 tax period. This tax reduction will directly reduce the revenue from corporate income tax in 2022 for the temporary payment for the fourth quarter and additional payment after tax finalization in 2021 and remittance to the state budget in 2022.

The tax departments also need to proactively assess the impact on state budget revenue in 2022 according to the following plan: 30% reduction of land rent and water surface rent in 2022 for organizations, units, enterprises and households and individuals are directly leased by the State under a decision or contract or a certificate of land use rights, ownership of houses and other land-attached assets of a competent state agency by annual payment of land rent.

Regarding revenue management, the local tax departments must estimate revenue in 2022 and consider factors increasing revenue by enhancing revenue management and combating revenue loss, and recovering tax debts; strengthening inspection and control of tax declaration and payment and tax refund; reviewing projects that have expired corporate income tax incentives; collect tax from e-commerce, digital-based business and other services of overseas suppliers who do not have a permanent business establishment in Vietnam.

For revenues from new production capacity, contractor taxes and projects that have expired corporate income tax exemption or reduction and revenues from e-commerce business activities, the General Department of Taxation requires the tax departments to project budget revenues from contractor taxes for new investment projects in the area and new revenues for finished projects which are about to go into production and business from 2023.

Regarding revenues related to houses, land and other budget revenues, the tax departments should follow the plans on land use right allocation, land use right auction at their localities and the plan on rearranging and handling of houses and land according to the provisions of Decree 167/2017/ND-CP to determine the revenue from houses, land and other revenues.

| Budget collection while preventing of budget revenue loss |

For revenues from dividends and profits distributed to the state capital invested in enterprises, the tax departments shall review and estimate the full revenues from dividends and profits to be distributed to each enterprise according to the provisions of Circular 85/2021/TT-BTC.

Related News

Hai Phong Customs sets new record in revenue of VND70,000 billion

07:45 | 31/12/2024 Customs

Stimulate production and business, submit to the National Assembly to continue reducing 2% VAT

15:47 | 02/12/2024 Finance

Abolishing regulations on tax exemption for small-value imported goods must comply with international practices

13:54 | 15/11/2024 Regulations

Budget revenue is about to be completed for the whole year estimate

08:34 | 13/11/2024 Finance

Latest News

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance

Tax policies drive strong economic recovery and growth

07:55 | 31/12/2024 Finance

E-commerce tax collection estimated at VND 116 Trillion

07:54 | 31/12/2024 Finance

More News

Big 4 banks estimate positive business results in 2024

13:49 | 30/12/2024 Finance

Flexible and proactive when exchange rates still fluctuate in 2025

11:03 | 30/12/2024 Finance

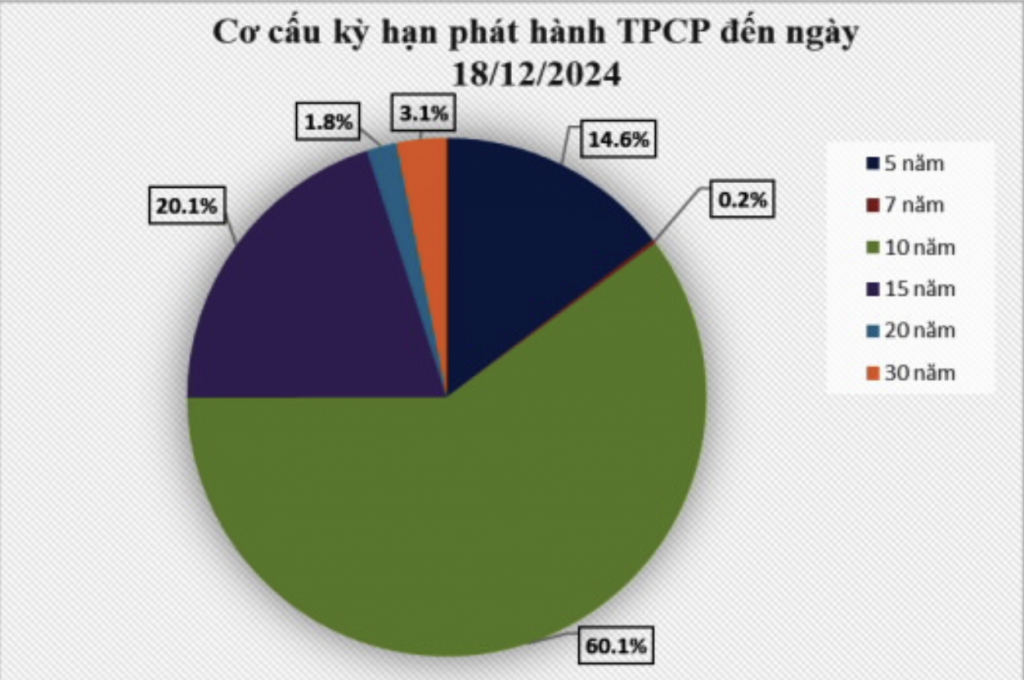

Issuing government bonds has met the budget capital at reasonable costs

14:25 | 29/12/2024 Finance

Bank stocks drive market gains as VN-Index closes final Friday of 2024 on a positive note

17:59 | 28/12/2024 Finance

Banks still "struggling" to find tools for handling bad debt

13:47 | 28/12/2024 Finance

Forecast upbeat for banking industry in 2025

14:30 | 27/12/2024 Finance

Ensuring financial capacity of bonds issuers

11:09 | 26/12/2024 Finance

Finance ministry announces five credit rating enterprises

14:54 | 25/12/2024 Finance

The capital market will see positive change

09:44 | 25/12/2024 Finance

Your care

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance

Tax policies drive strong economic recovery and growth

07:55 | 31/12/2024 Finance

E-commerce tax collection estimated at VND 116 Trillion

07:54 | 31/12/2024 Finance

Big 4 banks estimate positive business results in 2024

13:49 | 30/12/2024 Finance