Amending Circular 38/2018/TT-BTC: Codifying commitments on C/O in CPTTP

| Forum discusses press - businesses ties in CPTTP era | |

| Implementing CPTTP: How does Vietnam cut tariff? | |

| CPTTP – challenges for Vietnamese businesses |

|

| Customs operation at Noi Bai International Airport Customs Branch. Photo: N.L |

Head of a Division under Customs Control and Supervision Department Hoang Thi Thuy said that due to different contents of the CPTTP agreement, the instruction contents are regulated in a separate provision to create favourable condition for the Customs and businesses to implement. However, the general principle of checking and determining the origin of exported and imported goods still comply with the provisions of Circular 38/2018 / TT-BTC of the Ministry of Finance.

Specifically, contents that have been codified in commitments in the CPTTP agreement on checking and determining the goods origin of the Customs include: Origin rules in the CPTTP agreement (including three parts: 32 Articles, four appendixes and two sub-appendixes). Part A stipulates origin rules, including 18 articles on origin rules such as originating goods, wholly obtained goods, qualifying value content, calculation of materials and accumulation. Part B regulates procedures for origin determination, including 13 articles regulating declaration to apply special preferential tax rate, the form of certificate of origin. Part B provides regulations on other matters including a provision on the Commission for enforcement of origin rules and procedures for determining origin.

Regarding the four appendixes, appendix 3A stipulates other agreements (the self-certification of origin mechanism that C/O is issued by exporters or issued by competent agencies of the exporting country); Appendix 3B provides information on C/O of goods; Appendix 3C stipulates Exception of Article 3.11 on De minimis rule; Appendix 3D stipulates the product specific rules (PSR). In addition, the two sub-appendices include articles related to the rule of origin for vehicles, parts of vehicles and a sub-appendice of commodities in the list of lacked goods.

The Ministry of Finance will codify the provisions of the CPTPP with the contents related to procedures, methods of determining origin, including provisions related to the Customs authority at the draft circular amending and supplementing Circular 38/2018/TT-BTC.

The conditions for goods to enjoy special preferential tax rates under CPTPP for imported goods must be in the special preferential tariffs; exported from member states of the agreement, meet rules on freight (direct consignment); submit valid certificates of origin to customs authorities. For export goods, the condition for goods to enjoy special preferential tax rates under CPTPP is under the CPTPP export tariff; exported from Vietnam and imported into other member countries of CPTPP.

Certificate of origin includes: Certificate of goods origin issued by exporters and producers; C/O issued by competent agencies of the exporting country.

The minimum information of the self-certification of origin includes: exporter or producer, name or address (including country), phone number and e-mail address of exporter if the exporter is not a certifier; name, address (including country), phone number and e-mail address of producer if the producer is not a certifier or exporter; name, address, phone number and e-mail address of importer; description and HS code of goods, origin criteria, the time limit, date, month, year and authorised signatory.

C/O is issued for goods imported once, or the identical goods imported many time in the period on C/O but not more than 12 months from the date of issuing C/O. The identical goods must be imported by the same importer.

| Circular amending and supplementing Circular 38/2015 / TT-BTC: Many new regulations on management of processed goods and export production VCN- Regarding the Customs management of processed goods, export production and export processing enterprises, the Circular amending ... |

The draft circular also stipulates that Customs authorities shall accept C/O to apply special preferential tax rates if the invoice issued by a country that is not the member country. If the invoice is issued by a country that is not the member country, the self-certification of origin must be issued separately from that commercial invoice.

The time limit for submission of C/O, Customs declarant shall submit C/O at the time limit of carrying out customs procedures. If C/O is not issued at this time limit, customs declarant shall submit C/O and implement additional declaration within one year from the date of Customs declaration registration. If goods are subject to import management regimes, the time limit for submitting of C/O is the time of carrying out customs procedures. The time limit for carrying out customs procedures is determined from the time of registration to the time of Customs clearance. If the goods release time is different from Customs clearance time, the time limit for carrying out customs procedures is determined from Customs declaration registration time to the goods release time.

Related News

Halal Market: The Door is Wide Open, How to Exploit It

14:23 | 29/12/2024 Import-Export

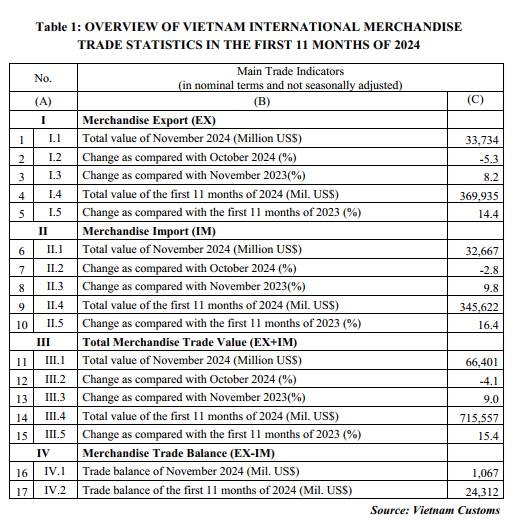

Preliminary assessment of Vietnam international merchandise trade performance in the first 11 months of 2024

10:50 | 27/12/2024 Customs Statistics

Goods trading, being seen from Lang Son border gate

13:45 | 28/11/2024 Customs

7 key export groups bring in US$234.5 billion

13:54 | 28/11/2024 Import-Export

Latest News

From January 1, 2025: 13 product codes increase export tax to 20%

14:23 | 29/12/2024 Regulations

Export tax rates of 13 commodity codes to increase to 20% from January 1, 2025

13:46 | 28/12/2024 Regulations

Proposal to reduce 30% of land rent in 2024

14:58 | 25/12/2024 Regulations

Resolve problems related to tax procedures and policies for businesses

13:54 | 22/12/2024 Regulations

More News

New regulations on procurement, exploitation, and leasing of public assets

09:17 | 15/12/2024 Regulations

Actively listening to the voice of the business community

09:39 | 12/12/2024 Customs

Step up negotiations on customs commitments within the FTA framework

09:44 | 08/12/2024 Regulations

Proposal to amend regulations on goods circulation

13:45 | 06/12/2024 Regulations

Review of VAT exemptions for imported machinery and equipment

10:31 | 05/12/2024 Regulations

Customs tightens oversight on e-commerce imports

13:39 | 04/12/2024 Regulations

Bringing practical experience into customs management policy

13:48 | 03/12/2024 Regulations

Businesses anticipate new policies on customs procedures and supervision

15:41 | 29/11/2024 Regulations

Do exported foods need iodine supplementation?

11:06 | 29/11/2024 Regulations

Your care

From January 1, 2025: 13 product codes increase export tax to 20%

14:23 | 29/12/2024 Regulations

Export tax rates of 13 commodity codes to increase to 20% from January 1, 2025

13:46 | 28/12/2024 Regulations

Proposal to reduce 30% of land rent in 2024

14:58 | 25/12/2024 Regulations

Resolve problems related to tax procedures and policies for businesses

13:54 | 22/12/2024 Regulations

New regulations on procurement, exploitation, and leasing of public assets

09:17 | 15/12/2024 Regulations