A Resolution on tax debt remission will be submitted to the National Assembly session in October 2019

|

| Photo. Thuy Linh. |

Many subjects will be considered for tax debt remission

On the afternoon of March 13, 2019, in the framework of the meeting of the Standing Committee of the National Assembly, the Minister of Finance Dinh Tien Dung said that through synchronous and drastic implementation of measures to recover outstanding tax debts, the proportion of total debt on total domestic revenue has dropped sharply from 12.2% in 2014 to 7.6% in 2017, and only 7% at the end of 2018.

However, the outstanding tax debts are still remarkable, the total tax debts as of December 31, 2017 was VND 78,466 billion, down by 2.8% (VND 2,261 billion) compared to December 31, 2016. Under the management of the tax authorities, the irrecoverable tax debts by taxpayers that have died, are missing, lost civil act capacity, are involved in criminal responsibility, have dissolved themselves, are insolvent, or have stopped and left their business address were VND 31,469 billion (original tax debts were VND 19,196 billion, fines and late payment interests were VND 12,273 billion), accounting for 43% of total tax debts, equal to 3.2% of total domestic revenue in 2017.

Under the Customs management, irrecoverable tax debts were VND 3,834 billion, accounting for 72% of the total debts, of which 43.2% of the debts are bad debts arising before the effective date of revised Law on tax administration.

Through the assessment of the actual situation, in order to resolve all outstanding debts, the Government requested the National Assembly to issue a Resolution on handling tax debts. If approved by the National Assembly, the Resolution is expected to take effect from July 1, 2019 and is applied within 5 years from the effective date.

Accordingly, there is no charge for late payment of tax debts and other amounts payable to the state budget, including the revenues from land rents and land use fees in some cases (specified in the Resolution). That is when the owner of a private enterprise or the owner of a one-member limited liability company is an individual and the taxpayer is an individual who has died or deemed dead, is missing, or lost civil act capacity, or limited civil act capacity, without assets to pay taxes and fines.

The second case is that the taxpayer has a dissolution decision sent to the tax administration agency and the business registration agency for the dissolution procedures, the business registration agency has informed that the taxpayer is making procedure for the dissolution on the National Information Portal on business registration, but the taxpayer has not completed the dissolution procedures.

The time of charge exemption for late payment is from the date when the business registration agency informs that the taxpayer is making procedures for the dissolution on the National Information Portal on the business registration.

The other cases are: Taxpayers that have submitted applications for opening bankruptcy procedures, or are forced to submit application for opening bankruptcy procedures by other people; taxpayers that no longer do business at the business address registered with the business registration agency and the tax administration agency in coordination with the commune, ward or township, People's Committee or the ward, commune’s tax advisory council, or the police office in the locality where the business address is registered, and the taxpayer’s contact address information has been checked and verified that the taxpayer does not operate at the registered business address and contract address registered with the tax administration agency ...

The Government also proposes remission of debts of late payment fees and fines before January 1, 2019, and exempt late payment fees arising from January 1, 2019 to the effective date of revised Law on Tax administration, of taxpayers who encounter natural disasters, fires, unexpected accidents, serious illnesses or other force majeure cases.

Also according to the Government’s proposal, tax debts, fines, late payment fines, late payment arising before January 1, 2019 for taxpayers in cases: Where enterprises or organizations have stopped production and business, but failed to fulfil the procedures for bankruptcy and dissolution in accordance with law and have no money in accounts opened at banks, no assets at the registered business address, and have no signs of dispersing assets before the time of dissolution or bankruptcy; where business households and individuals face difficulties and have stopped their business and failed to pay the tax debt amounts, and no longer do business and production activities at the registered business address, or have been revoked business registration certificate by competent authorities.

Consider debt remission for some subjects who do not comply with regulations

Agreeing with the necessity to issue the Resolution, however, through an investigation, the Chairman of the National Assembly's Finance - Budget Committee Vu Duc Hai said that the draft Resolution stipulates the fee exemption for late payment for "Taxpayers no longer doing business at the business address registered with the business registration agency ... ". This provision may be a loophole for taxpayers to take advantage of, by removing registered business address and moving to another area, or establishing a new legal entity at another address for tax evasion. If they are discovered by the state agency after many years and asked for payment of arrears, the tax debts is still equal to the tax debts at the time of removing the business address. Therefore, it is recommended to consider the debt remission and exemption for late payment fines for these cases.

At the same time, it is also recommended to consider the handling of tax debts for state-owned enterprises in the process of equitization and restructuring of state-owned enterprises. Also, the Government is requested to supplement tables and figures on tax debt situation and specifically classified tax debts by ownership form (individual households, private enterprises, state-owned enterprises, FDI enterprises ...); by competence of tax debt remission (the Minister of Finance, the General Department of Taxation, the General Department of Customs; chairmen of provincial-level People's Committees); by subjects of debt remission (tax money, late payment, late payment fine ...)

Affirming the necessity of issuance of the Resolution, but the National Assembly Chairman Nguyen Thi Kim Ngan also requested the drafting board verify and review the provisions so that these provisions shall not be abused and create a bad precedent for the subjects deliberately delaying the payment and evading tax.

National Assembly Vice Chairman Phung Quoc Hien said that if all the contents proposed by the Government are approved, the debts which shall be removed, shall be VND 27 to 31 trillion, equivalent to US$ 1.5 billion, so it must be considered carefully.

"It is necessary to build a Resolution in a careful, serious and lawful manner, avoiding consequences related to tax and other policies such as credit, loans ... At the same time, there should be a responsibility assessment of taxpayers, tax administration agencies, authorities. Development of this Resolution is to reduce the tax debt rate to a low level which is in the permitted rate and prevent tax fraud and evasion,” said Hien.

Appreciating the comments of the Standing Committee of the National Assembly, Minister of Finance Dinh Tien Dung committed to build the contents of the Resolution in a spirit of transparency and fairness, ensuring the strictness of the tax law.

| The arduous process of recovering import and export tax debts – Part 4: There should be a mechanism for tax debt remission VCN - As mentioned in the previous articles, the tax debt situation from 2013 and earlier, has ... |

The Standing Committee of the National Assembly decided to submit the Resolution to the National Assembly for consideration and approval of the revised Law on Tax Administration. Accordingly the Government will base the approved law and comments of the Finance –Budget Committee, the Standing Committee of the National Assembly and the Government, to consider and supplement the Resolution to the 2019 legislative program of the National Assembly and submit it to the National Assembly at the 8th session in October 2019.

Related News

Numerous FDI enterprises face suspension of customs procedures due to tax debt

09:57 | 18/12/2024 Anti-Smuggling

Vietnam makes comprehensive strides in public financial management reform

09:16 | 01/12/2024 Finance

Major reforms in the management of state capital in enterprises

09:18 | 01/12/2024 Finance

Revising the title of a draft of 1 Law amending seven finance-related laws

14:33 | 21/11/2024 Finance

Latest News

SBV makes significant net withdrawal to stabilise exchange rate

07:59 | 15/01/2025 Finance

Việt Nam could maintain inflation between 3.5–4.5% in 2025: experts

06:19 | 11/01/2025 Finance

Banking industry to focus on bad debt handling targets in 2025

14:38 | 03/01/2025 Finance

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

More News

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance

Tax policies drive strong economic recovery and growth

07:55 | 31/12/2024 Finance

E-commerce tax collection estimated at VND 116 Trillion

07:54 | 31/12/2024 Finance

Big 4 banks estimate positive business results in 2024

13:49 | 30/12/2024 Finance

Flexible and proactive when exchange rates still fluctuate in 2025

11:03 | 30/12/2024 Finance

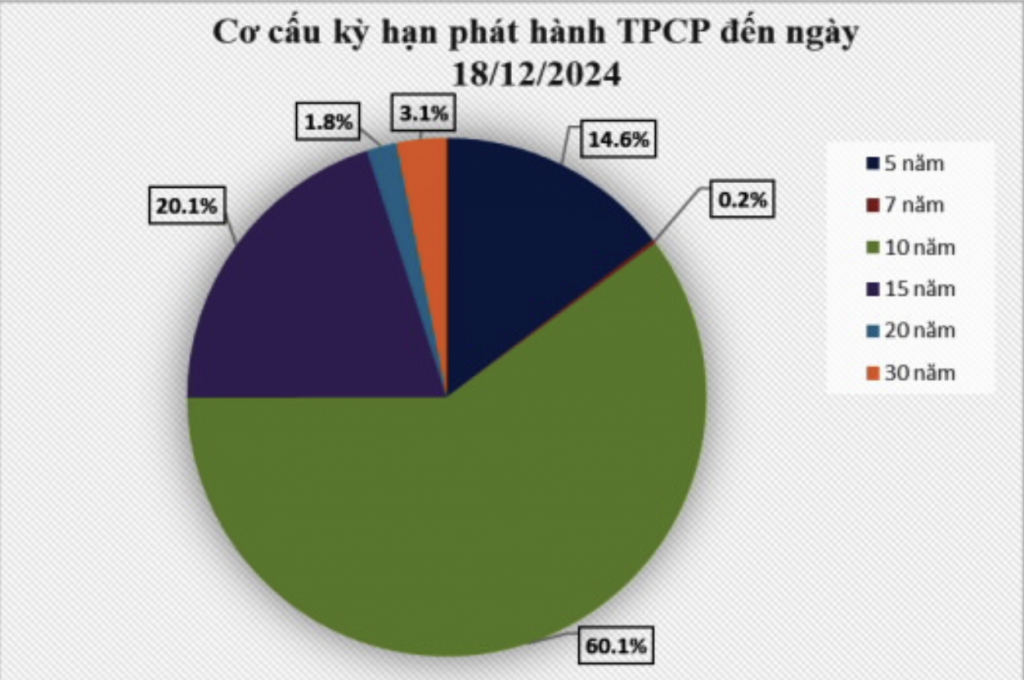

Issuing government bonds has met the budget capital at reasonable costs

14:25 | 29/12/2024 Finance

Bank stocks drive market gains as VN-Index closes final Friday of 2024 on a positive note

17:59 | 28/12/2024 Finance

Banks still "struggling" to find tools for handling bad debt

13:47 | 28/12/2024 Finance

Forecast upbeat for banking industry in 2025

14:30 | 27/12/2024 Finance

Your care

SBV makes significant net withdrawal to stabilise exchange rate

07:59 | 15/01/2025 Finance

Việt Nam could maintain inflation between 3.5–4.5% in 2025: experts

06:19 | 11/01/2025 Finance

Banking industry to focus on bad debt handling targets in 2025

14:38 | 03/01/2025 Finance

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance