There is no traditional taxi tax or charge that is higher than Uber and Grab

|

| Uber, Grab take obligation under the turnover entitled. Picture: The Internet |

The policy has been unified

In practice, the current tax law is applied uniformly among types of enterprises (uniform tax rates, conditions for investment incentives, tax exemption and reduction...).

Accordingly, the current tax law is applied uniformly among types of enterprises. If the enterprise determines the revenue, expenses, and income of its business activities, it will pay tax by the declaration method.

The method of ratio on taxable turnover is only applied to foreign contractors who do not meet the conditions for tax payment by the declaration method, and organizations which are not enterprises or enterprises that pay value added tax under the direct method, business individuals involved in goods or service business activities, which can determine turnover but can not determine expenses and incomes of business activities.

Specifically, Uber B.V Netherlands Co., Ltd does not meet the conditions for paying VAT by the deduction method and fails to meet business income tax on the basis of the declaration of turnover and expenses for determination of taxable income of its business activities.

Under the current regulations, the tax obligations of Uber B.V Netherlands are defined that: The percentage for calculating the VAT on turnover is 3%; The percentage for calculating the business income tax on turnover is 2%.

For transport business organizations (enterprises, cooperatives) established under the law having contracts with Uber BV Netherlands for business is obliged to declare and pay VAT, CIT for the portion of income received under the contract (excluding the revenue of Uber BV Netherlands).

If the individual signs a contract with Uber Holland BV for business transport, the tax liability is 3% of the turnover to calculate VAT and 1.5% of the revenue to calculate the personal tax.

For Grab transport business activities, the General Department of Taxation has also sent instructions to Tax Departments of some provinces and cities implementing this model guiding the tax policy to be implemented uniformly under the principle of turnover-sharing business cooperation contract as applied to Uber.

There is no basis for tax deduction for traditional taxis

For traditional taxis, the Tax Policy Department says that some traditional taxis offer to be applied the tax as guided for Uber, Grab, or traditional taxpayers are allowed to pay VAT at the rate of 5% instead of the current 10%; At the same time, it is recommended that the taxable income for Uber and Grab must be on the basis of 100% revenue.

However, the current tax law stipulates: For the method of deduction of VAT, the enterprise will apply the VAT rate of 10% for transport services and the VAT will be equal to the output VAT minus input VAT.

Therefore, when determining the VAT, the enterprise is entitled to VAT deduction of input costs (such as office expenses, repair costs, purchase of fixed assets ...).

According to the Tax System Reform Strategy in the period 2011-2020, the VAT rate will gradually be applied to the uniform application of 10%, the tax rate of 5% will apply only to essential goods and the tax rate of 0% will be applied to the export goods. Therefore, the proposal "for a traditional tax to pay VAT at the rate of 5%" is unwarranted.

For corporate income tax, all revenue from transportation business must be declared and pay tax. For each organization or individual engaged in transport business in the form of a turnover-sharing business cooperation contract, it is obliged to pay tax on the turnover divided according to the cooperation agreement.

If determining Uber and Grab’s tax revenue of 100% of the revenue earned from the customer, it would be overlapping and unreasonable taxation, because of the 100% of Uber's revenue from the customer, Uber is only entitled 20% of transportation revenue; the remaining 80% of transportation revenue is divided to organizations and individuals cooperating with Uber under the agreement of business cooperation contract and these organizations and individuals must declare and pay tax as prescribed for the revenue entitled.

According to the data of the tax branch, in Ho Chi Minh City, of the 10 enterprises with large turnover, 2 enterprises generated VAT that are deducted, not generated VAT payable (Mai Linh Travel Co., Ltd, Thanh Buoi Co., Ltd), other companies with the rate of VAT/turnover less than 3% (Gia Dinh Joint Stock Company, Saigon Tourist Transport Company, Transport Co-operative No. 10).

On the CIT, most enterprises have a low tax/turnover propotion, or not generates CIT taxpayble, the tax rate is 0.01%-0.06%. Anh Duong Co., Ltd alone, the CIT rate is 1.97%/revenue (equivalent to theh Uber).

With the information that "traditional taxis are subject to a lot of taxes, charges with tax rates are quited different to the Grab, Uber" is not true. The Ministry of Finance is directing the General Department of Taxation to review cases showing signs of tax fraud risk for handling in accordance with the law.

Related News

Minister of Finance: continue to advise on promulgating fiscal policies to help economy recover and develop

15:15 | 08/07/2024 Finance

Studying, guiding implementation of new policies on microinsurance

09:52 | 26/08/2022 Finance

Ministry of Finance proposes to reduce rates of fees and charges in 2022

10:36 | 26/11/2021 Finance

Ho Chi Minh City Taxi Association: Grab has got benefits for itself

17:00 | 19/12/2020 Finance

Latest News

Debt repayment pressure continues to weigh on corporate bond market

14:11 | 20/01/2025 Finance

2025 a new era for financial institutions

16:49 | 19/01/2025 Finance

Positive outlook for Việt Nam’s banking sector in 2025

08:04 | 16/01/2025 Finance

SBV makes significant net withdrawal to stabilise exchange rate

07:59 | 15/01/2025 Finance

More News

Việt Nam could maintain inflation between 3.5–4.5% in 2025: experts

06:19 | 11/01/2025 Finance

Banking industry to focus on bad debt handling targets in 2025

14:38 | 03/01/2025 Finance

State Bank sets higher credit growth target for 2025

15:22 | 31/12/2024 Finance

Outlook for lending rates in 2025?

15:20 | 31/12/2024 Finance

Tax policies drive strong economic recovery and growth

07:55 | 31/12/2024 Finance

E-commerce tax collection estimated at VND 116 Trillion

07:54 | 31/12/2024 Finance

Big 4 banks estimate positive business results in 2024

13:49 | 30/12/2024 Finance

Flexible and proactive when exchange rates still fluctuate in 2025

11:03 | 30/12/2024 Finance

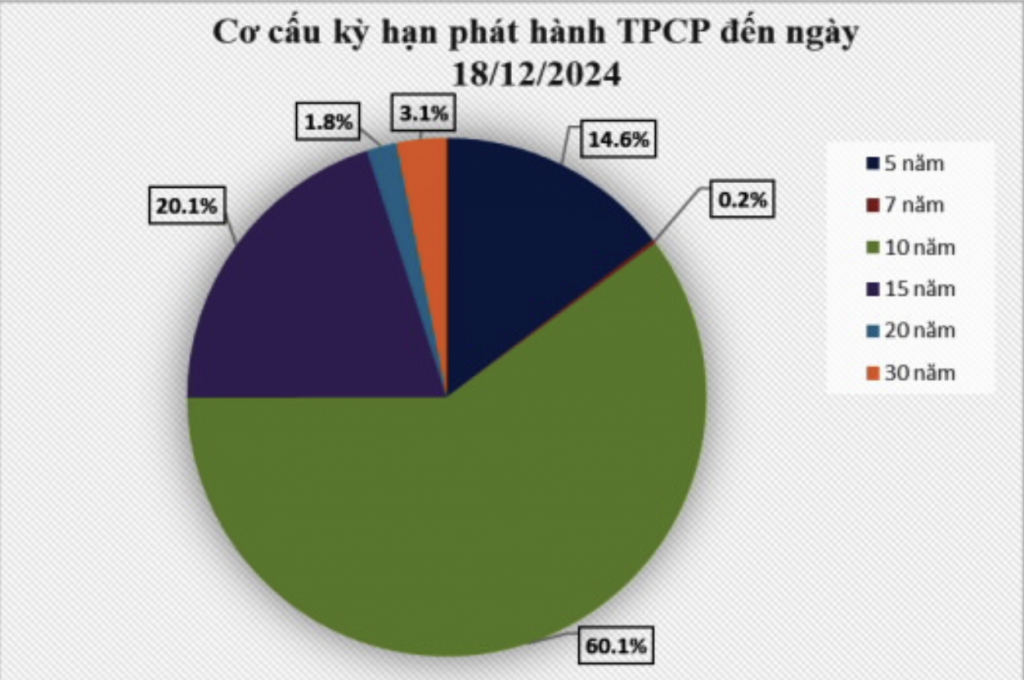

Issuing government bonds has met the budget capital at reasonable costs

14:25 | 29/12/2024 Finance

Your care

The system has not recorded your reading habits.

Please Login/Register so that the system can provide articles according to your reading needs.

Debt repayment pressure continues to weigh on corporate bond market

14:11 | 20/01/2025 Finance

2025 a new era for financial institutions

16:49 | 19/01/2025 Finance

Positive outlook for Việt Nam’s banking sector in 2025

08:04 | 16/01/2025 Finance

SBV makes significant net withdrawal to stabilise exchange rate

07:59 | 15/01/2025 Finance

Việt Nam could maintain inflation between 3.5–4.5% in 2025: experts

06:19 | 11/01/2025 Finance