Banks seek medium and long-term capital

| Banks rush to raise capital through bond issuance | |

| Banks may assess pollution risks before granting loans | |

| Banks are struggling to sell collateral |

|

| Reducing the ratio of short-term capital used for medium and long-term loans will reduce risks for banks. |

Issuing bonds, certificates of deposit

At the end of May, ACB’s Board of Directors approved a plan to issue individual bonds in the second half of 2019 totaling VND5,500 billion with terms of 2-3 years.

The bonds will be issued in five installments according to the method of issuing agents.

The interest rate applicable to bonds is a fixed interest rate during the issuing period, depending on market conditions and investors' demand, but not exceeding 6.75% per year for the three-year term and 6.7% for two-year term.

InApril, ACB's Board of Directors also approved aplan toissue individual bonds in the first half of 2019 with a value of VND2,500 billion. Similarly, Vietinbank has just receivedapproval from the SBV to issue bonds in 2019 with a total value of VND10,000 billion. Currently, Vietinbankholds more than VND32,000 billion in bonds, of which bonds with terms of over 5 years total VND26,515 billion.

In addition to issuing bonds, many banks are also promoting the issuance of certificates of deposit with interest rates much higher than normal deposit rates.From now until the end of September, VietABank will issue registration certificates of deposit with interest rates of up to 9.1% per year with end-of-term interest and 8.38% per year in the form of monthly interest.

SHB bankisalso offering interest rates of up to 8.9% per year for deposit certificates for individual customers and businesses. The total value of the issue is VND10,000 billion. Accordingly, individuals can purchase certificates of under VND2 billion, interest rates applicable to terms of 18, 24 and 36 months are 8.6%, 8.7% and 8.8% per year, respectively.

With certificates valued at VND2 billion or more, the applicable interest rates are 8.7%, 8.8% and 8.9% per year, respectively. At Sacombank, individual and institutional customers buy long-term deposit certificates with a minimum par value of VND1 million, a seven-year term (84 months) is entitled to an interest rate of 8.6% per year. Similarly, BIDV bank also has a medium and long-term deposit certificate program from early March with an interest rate of 7.6% per year for fixed interest rates and 7.5% per year for floating interest rates. LienVietPostBank has a program to mobilize capital throughcertificates of deposit for terms of 15 months, 18 months, 24 months and 36 months with an interest rate of 8.1% per year (higher than the interest rate of savings deposits of the same termby0.7 to 1% per year).

Capital structure

According to the draft replacing Circular 36/2014/TT-NHNN regulating the limits and safe ratios in the operation of banks and foreign branches given for comments, there are two ways to reduce the ratio of short-term capital used formedium and long-term loans bycredit institutions.

According to the first option, the maximum ratio of short-term funds used for medium and long-term loans is maintained at 40% by the end of June 30, 2020; then decreases gradually to 30% on July 1, 2021. In the second option, the reduction route will be more relaxed. The deadline for bringing the ratio of short-term capital to medium and long-term loans to 30% will be moved to July 1, 2022.

Accordingly, the fact that many commercial banks are promoting the mobilization of medium and long-term capital, including the issuance of bonds and certificates of deposit, demonstrates the initiative of banks to prepare for the above roadmap.

In recent years, banks have also continuously increased their charter capital to increase the scale of financial potential to expand their business. Many banks also look to other forms such as foreign loans, access to entrusted funding sources to international organizations, or through the stock market.

According to the State Bank, the ratio of short-term capital used for medium and long-term loans of the whole system is only 28.42%. Specifically, the State-owned commercial banks are currently at 31.12%, whilejoint-stock commercial banks are 32.4%, much lower than the current regulations. However, this is only an average; in fact, this rate atmany banks is quite high.

| Banks speed up resolving bad debts Commercial banks have been proactive in handling bad debts with many posting an increasing ratio. |

Specifically, according to thefirst quarter of 2019’s financial statements, the proportion of medium and long-term credit in Techcombank's total outstanding loans is nearly 63%, in VPBank is nearly 66%, Sacombank is 51% and SHB is 59%.

The high proportion of medium and long-term credit means the ratio of short-term capital used for medium and long-term loans will also be high.

Speaking at the recent Private Economic Forum, Deputy Governor of the State Bank Dao Minh Tu said that the medium and long-term capital source for the economy still relies heavily on the banking system.Medium and long-term credit accounts for about 50.6% of total outstanding loans. This creates great pressure and risks for the credit institution system. With this situation, financial and banking experts all evaluated that the reduction of the use of short-term capital for medium and long-term loans to 30% is in line with international practices because currently in many developed countries, this coefficient is currently only at 20%. Pulling down this ratio will reduce banks' risks.

In addition, the period from now until2021 (in the first option) or 2022 (according to the second option) is considered to be enough time for banks to arrange and restructure their capital.

Related News

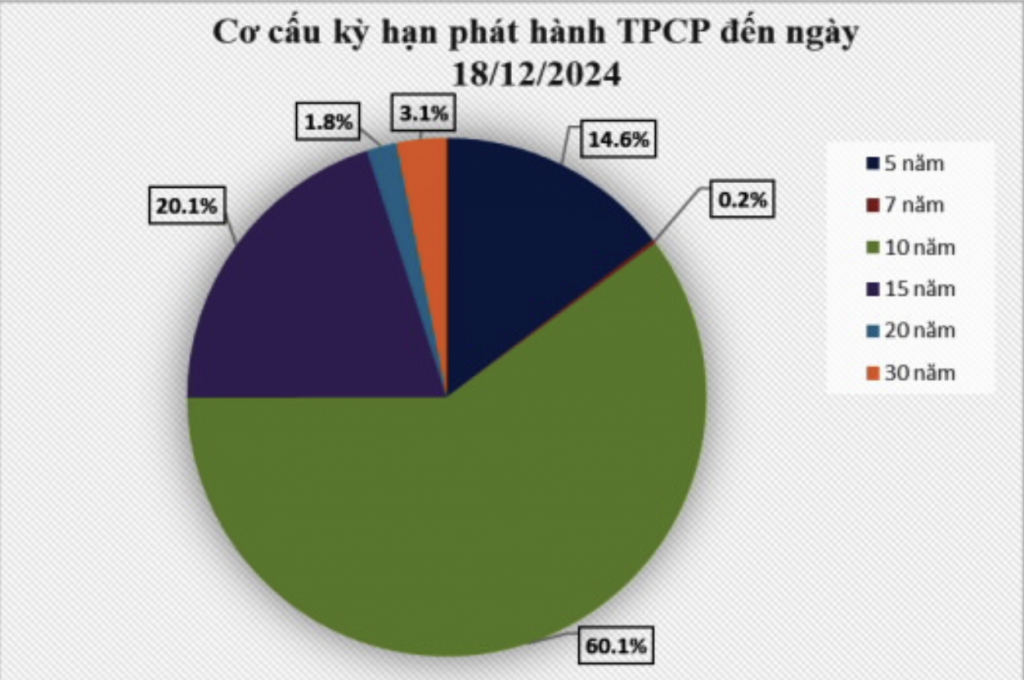

Issuing government bonds has met the budget capital at reasonable costs

14:25 | 29/12/2024 Finance

Untying the knot for green finance

11:08 | 23/12/2024 Finance

Publicizes progress of public investment disbursement for important national projects

15:21 | 19/12/2024 Finance

Banks increase non-interest revenue

10:51 | 23/11/2024 Finance

Latest News

Việt Nam tightens fruit inspections after warning from China

08:01 | 15/01/2025 Import-Export

Brand building key to elevate Vietnamese fruit and vegetable sector: experts

08:00 | 15/01/2025 Import-Export

Freight transport via China-Việt Nam cross-border trains posts rapid growth

08:01 | 13/01/2025 Import-Export

Vietnamese retail industry expects bright future ahead

06:22 | 11/01/2025 Import-Export

More News

Complying with regulations of each market for smooth fruit and vegetable exports

13:06 | 09/01/2025 Import-Export

Fruit and vegetable industry aims for $10 billion in exports by 2030

15:12 | 07/01/2025 Import-Export

GDP grows by over 7 per cent, exceeds target for 2024

15:11 | 07/01/2025 Import-Export

Vietnamese pepper: decline in volume, surge in value

15:10 | 07/01/2025 Import-Export

Việt Nam maintains position as RoK’s third largest trading partner

15:09 | 07/01/2025 Import-Export

Greater efforts to be made for stronger cooperation with European-American market

15:08 | 06/01/2025 Import-Export

Leather, footwear industry aims to gain export growth of 10% in 2025

15:06 | 06/01/2025 Import-Export

Grasping the green transformation trend - A survival opportunity for Vietnamese Enterprises

14:53 | 06/01/2025 Import-Export

Việt Nam to complete database of five domestic manufacturing industries in 2026

20:57 | 05/01/2025 Import-Export

Your care

Việt Nam tightens fruit inspections after warning from China

08:01 | 15/01/2025 Import-Export

Brand building key to elevate Vietnamese fruit and vegetable sector: experts

08:00 | 15/01/2025 Import-Export

Freight transport via China-Việt Nam cross-border trains posts rapid growth

08:01 | 13/01/2025 Import-Export

Vietnamese retail industry expects bright future ahead

06:22 | 11/01/2025 Import-Export

Complying with regulations of each market for smooth fruit and vegetable exports

13:06 | 09/01/2025 Import-Export