Amending the method for customs valuation of imported goods

|

| In fact, there are many cases of deliberately excluding software of imported machinery and equipment from those machinery and equipment so as not to add it to the transaction value. Illustrated photo |

Imported goods containing software

The transaction value-based method for imported goods is stipulated in Article 6, Article 7 and Article 17 of Circular 39/2015/TT-BTC. Specifically, Clause 4, Article 6 of Circular 39/2015/TT-BTC regulates the determination of customs value of imported goods related to the import of software. According to the analysis of the drafting committee, these regulations only stipulate imported goods containing software but fail to clarify two contents: when the software is considered to determine the value together with imported machinery and equipment must be installed on those pieces of machinery and equipment, or installed on a connected computer system to control the operation of those pieces of machinery and equipment and the machinery and equipment cannot work without the software; and the cost of software use rights must be added to the customs value of imported goods.

In addition, Clause 4, Article 6 and Article 13 of Circular No. 39/2015/TT-BTC stipulates that customs value is the actual value paid or will have to be paid for imported goods including software and the cost to install software on imported goods. But these regulations do not solve the problem that software is not imported in the same shipment with machinery and equipment, so there is a gap for enterprises to transfer the value into separate import software to reduce the value of machinery and equipment, reducing tax payable. In point A, Clause 4, Article 6, there is a loophole for enterprises to take advantage to make documents and vouchers so as not to add the software value to the value of imported equipment.

The failure to limit the software in this case being software related to imported machinery and equipment leads to confusion with common software in software business and is a chance for customs declarants to deliberately exclude software from imported machinery and equipment.

In fact, there were cases where the Customs declarants declared imported equipment at a customs department and imported software at another customs department. There was a case where enterprises imported codes to use system control software but did not know how to determine customs value.

Regarding the Customs agency, the definition of adding or not adding the value of the software to the value of imported equipment also helps Customs officers in checking and determining the imported software, which is common application software or software related to other imported machinery and equipment, to prevent risks of insufficient declaration of customs value, especially when software can be very expensive.

Therefore, to overcome the above shortcomings, the drafting committee proposed to amend regulations on customs valuation of machinery and equipment related to imported software in the following directions: specifying that this content applies for goods as machinery and equipment containing software; and specifying situations subject to determination of software value to add to the transaction value of machinery and equipment; the customs agency instructs enterprises on the determination, declaration and the customs agency inspects the value of machinery and equipment related to imported software to meet the reality. This content is specified in Clause 5 of Article 1 in the draft Circular.

Special relationship in transactions

Clause 4, Article 7 of Circular 39/2015 / TT-BTC stipulates: "On the basis of the available information, if the special relationship is suspected to affect the transaction value, the customs agency shall make a notification and hold a dialog enabling the customs declarant to explain and provide the information clarifying such special relationship to prove that such relationship does not affect the transaction value of the imported goods prescribed.”

According to the drafting committee, through the actual management of customs valuation for these cases arise problems and shortcomings, because the determination of whether the purchase price is or is not affected by the special relationship requires the efforts of both the Customs and Customs declarants, in which the review and comparison of the declared information with the data of the Customs agency is very important.

According to WCO guidelines and advanced countries (the USA, the EU, Australia, New Zealand), if there is any doubt about the transaction value with a special relationship, customs officers may compare to determine whether the value is affected or is not affected by the special relationship. On the other hand, in the context of increasingly rich international trade conditions, the knowledge of customs officers is limited; customs officers shall meet more difficulties in checking evidence submitted by customs declarants.

Furthermore, with the current regulations, customs officers have the right to request customs declarants to submit documents and vouchers which are beyond the capacity of customs declarants (such as requirement on whole transaction documents saved by another enterprise) and customs officers use this reason to refuse customs value. This is a loophole for harassment in the management of customs value.

Therefore, to enhance the transparency of this regulation and facilitate customs declarants and customs officers to apply this regulation in practice in consistency with the general principle of customs valuation of imported goods mentioned in Article 5 of the Circular, Clause 4 Article 7 is proposed to be amended as follow:

Regulating the responsibility of customs officers in self-reviewing the database of the Customs sector to search for evidence proving that the special relationship does not affect the transaction value before requesting enterprises to present evidence.

Specifying documents and vouchers that enterprises have to submit to prove the special relationships and the formation of transaction value.

| Correct the collection of carriage charge in the customs valuation VCN – In order to stop the situation by some Customs Departments implementing the calculation of carriage ... |

Adding regulations on the relevant information and basis for accepting explanation of the enterprise to ensure the conclusion of the special relationship whether or not to affect to customs value. This content is detailed in Clause 6 Article 1 of the draft Circular.

Related News

Customs sector strengthens anti-smuggling for e-commerce products

19:09 | 21/12/2024 Anti-Smuggling

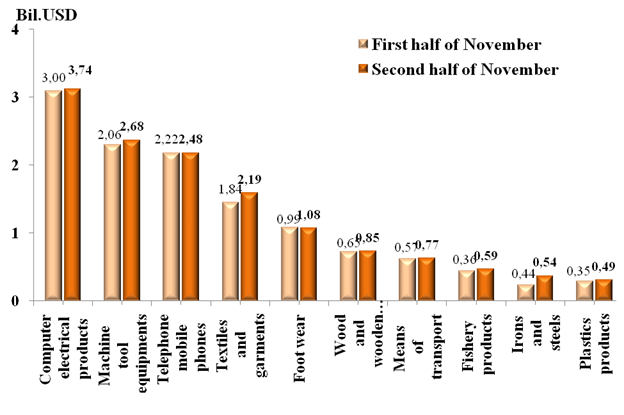

Preliminary assessment of Vietnam international merchandise trade performance in the second half of November, 2024

15:18 | 19/12/2024 Customs Statistics

Achievements in revenue collection are a premise for breakthroughs in 2025

09:57 | 18/12/2024 Customs

Ministry of Finance stands by enterprises and citizens

15:30 | 13/12/2024 Finance

Latest News

New regulations on procurement, exploitation, and leasing of public assets

09:17 | 15/12/2024 Regulations

Actively listening to the voice of the business community

09:39 | 12/12/2024 Customs

Step up negotiations on customs commitments within the FTA framework

09:44 | 08/12/2024 Regulations

Proposal to amend regulations on goods circulation

13:45 | 06/12/2024 Regulations

More News

Review of VAT exemptions for imported machinery and equipment

10:31 | 05/12/2024 Regulations

Customs tightens oversight on e-commerce imports

13:39 | 04/12/2024 Regulations

Bringing practical experience into customs management policy

13:48 | 03/12/2024 Regulations

Businesses anticipate new policies on customs procedures and supervision

15:41 | 29/11/2024 Regulations

Do exported foods need iodine supplementation?

11:06 | 29/11/2024 Regulations

Amendments to the Value-Added Tax Law passed: Fertilizers to be taxed at 5%

13:43 | 28/11/2024 Regulations

Proposal to change the application time of new regulations on construction materials import

08:52 | 26/11/2024 Regulations

Ministry of Finance proposed to reduce VAT by 2% in the first 6 months of 2025

09:00 | 24/11/2024 Regulations

Hanoi Customs resolves tax policy queries for enterprises

09:26 | 22/11/2024 Regulations

Your care

New regulations on procurement, exploitation, and leasing of public assets

09:17 | 15/12/2024 Regulations

Actively listening to the voice of the business community

09:39 | 12/12/2024 Customs

Step up negotiations on customs commitments within the FTA framework

09:44 | 08/12/2024 Regulations

Proposal to amend regulations on goods circulation

13:45 | 06/12/2024 Regulations

Review of VAT exemptions for imported machinery and equipment

10:31 | 05/12/2024 Regulations